Q4 2025 Market Review & 2026 Outlook

Dear Wela Clients,

As we begin 2026, we reflect on a remarkable final quarter of 2025 — one that defied expectations, stabilized global markets, and laid the groundwork for a more balanced year ahead.

Q4 brought a welcome shift from uncertainty to resilience. Inflation eased, interest rates turned lower, and long-feared tariff disruptions gave way to renewed trade stability. Investors who stayed patient through early-year turbulence were rewarded with a broad-based rally across equities, stronger fixed-income returns, and early signs of economic reacceleration.

The story of late 2025 was not one of unrestrained optimism, but of adjustment — markets learning to live, and even thrive, amid imperfection.

In this Market Outlook, we examine six defining themes that shaped the final months of the year and continue to influence the opening chapter of 2026:

1. The economy: resilience over recession

2. Tariff fatigue and market adjustment

3. Broadening growth and corporate earnings recovery

4. The Federal Reserve’s dovish pivot

5. Fixed income: income, defense, and opportunity

6. Equities: diversification returns

1) The Economy: Resilience Over Recession

If the first half of 2025 was marked by policy shocks and uncertainty, Q4 brought clarity — and with it, quiet strength.

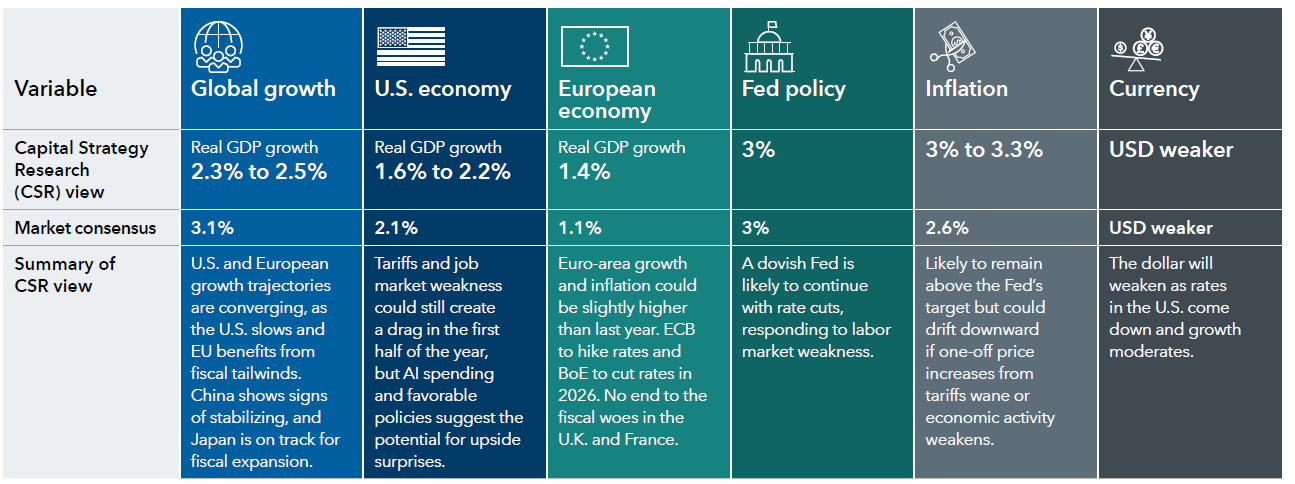

Despite fears of a late-cycle slowdown, global data in the final quarter pointed toward stabilization. The U.S. economy expanded at an estimated 1.7%–2.1% annualized rate, bolstered by steady consumer spending and industrial investment. Europe, long lagging, found fresh momentum through fiscal stimulus, while Asia — particularly Japan and China — showed signs of revival as trade flows normalized.

The so-called “Benjamin Button economy” persisted into year-end: a business cycle running in reverse, with conditions improving when most expected a downturn. Labor markets stayed firm, household balance sheets remained resilient, and corporate reinvestment picked up pace — particularly in industrials, infrastructure, and energy.

Inflation cooled further, averaging 3.1% in the U.S. and 3.3% in the Eurozone during Q4, even as wage growth stabilized. The result was a surprisingly soft landing: slower growth, but with renewed balance across sectors and regions.

The takeaway from Q4 2025? The global economy didn’t dodge a recession — it redefined resilience.

2) Tariff Fatigue and Market Adjustment

Few policy stories defined 2025 more than tariffs — and few ended on a calmer note.

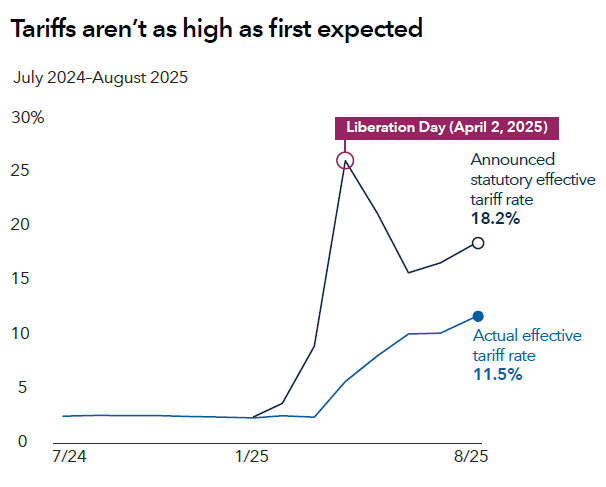

April’s “Liberation Day” triggered the largest tariff hike in modern U.S. history, rattling supply chains and investor confidence. But by Q4, the panic had faded. The effective U.S. tariff rate stabilized near 11%, far below the 18% statutory figure originally announced.

Behind the headlines, global trade adapted quickly. By late 2025:

• Nearshoring in Mexico and Eastern Europe had accelerated,

• Reshoring in U.S. semiconductor and defense manufacturing expanded, and

• Diversified trade deals with Asia-Pacific partners began to offset earlier friction.

The result was renewed corporate planning confidence. The Bloomberg Policy Uncertainty Index fell nearly 60% from its April highs, returning to pre-pandemic levels by December.

Q4 reminded investors that markets don’t fear tariffs — they fear uncertainty. Once the policy outlook steadied, fundamentals reclaimed control.

3) Broadening Growth and Corporate Earnings Recovery

Q4 2025 marked a turning point for corporate earnings — and for market breadth.

After a sluggish first half, global profits surged into year-end. Earnings growth for S&P 500 companies averaged double digits in Q4, while Europe and Japan delivered their strongest corporate profit gains since 2021.

The drivers were diverse:

• AI-driven productivity continued to lift margins,

• Infrastructure spending in Europe and the U.S. accelerated, and

• Global trade stabilization revived cyclical industries like materials and logistics.

Importantly, market leadership has broadened. Nearly 60% of S&P 500 constituents ended the year above their 200-day moving average — the widest participation since 2021.

The “Magnificent Seven” tech names, while still dominant, no longer carried the market alone. Industrials, energy, and financials all contributed meaningfully to Q4’s rally.

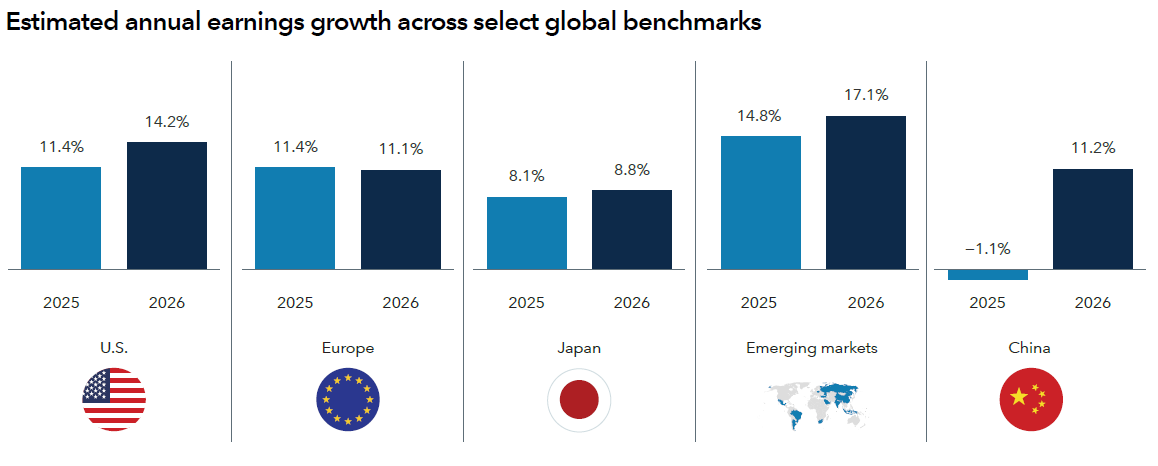

Earnings expectations for 2026 remain optimistic: +14% for the U.S., +11% for Europe, and +17% for emerging markets. The tone has shifted from “relief rally” to genuine recovery.

Still, caution is warranted. Equity valuations ended 2025 elevated — U.S. forward P/E ratios remain above their 10-year average. As 2026 begins, stock selection and disciplined rebalancing will be key.

4) The Federal Reserve’s Dovish Pivot

If tariffs dominated headlines in Q2 and Q3, the Federal Reserve stole the spotlight in Q4.

After nearly two years of restrictive policy, the Fed made a decisive shift in late 2025, initiating a measured easing cycle that brought the federal funds rate to roughly 3% by year-end.

Chair Powell emphasized a “soft landing” narrative, pointing to moderating inflation and emerging signs of labor market slack. Markets welcomed the move: both stocks and bonds posted strong Q4 gains, with investors interpreting the pivot as confirmation that the tightening cycle had achieved its goal.

Key effects of the Fed’s pivot in Q4 included:

• Mortgage demand ticked higher for the first time since 2021,

• Corporate credit spreads narrowed, and

• Treasury yields retreated, bolstering total returns across fixed income.

Historically, easing cycles outside recessions have boosted both equities and bonds — and Q4 followed that pattern. Investors who stayed diversified through volatility were rewarded as yields fell and risk assets rallied.

5) Fixed Income: Income, Defense, and Opportunity

Bonds quietly became one of Q4’s strongest performers.

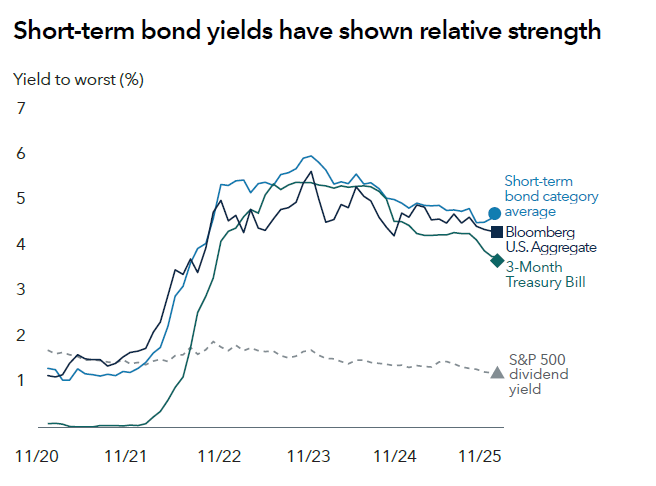

As the Fed turned dovish, bond prices rallied and yields stabilized near multi-year highs, offering investors both income and appreciation potential. The Bloomberg U.S. Aggregate Index returned solid single-digit gains in Q4 and entered 2026 yielding around 4.3%.

The fixed-income playbook that guided much of 2025 held true through year-end:

• Core Bonds: Continued to anchor portfolios and smooth volatility.

• Short-Term Bonds: Outperformed cash as yields compressed.

• Credit Opportunities: High-quality corporates and securitized credit benefited from narrowing spreads and low default rates.

• Municipal Bonds: After a challenging year, municipal bonds rebounded sharply in Q4, buoyed by strong demand for tax-advantaged income.

For the first time in nearly a decade, bond investors ended the year with both strong total returns and robust starting yields for the year ahead — a compelling setup for 2026.

6) Equities: Diversification Returns

Equity markets ended 2025 on a high note — but what stood out most was how they rallied.

Rather than a narrow tech surge, Q4 saw a broad-based advance across sectors and geographies. International markets, long overlooked, outperformed U.S. peers, driven by fiscal expansion in Europe and reform momentum in Asia.

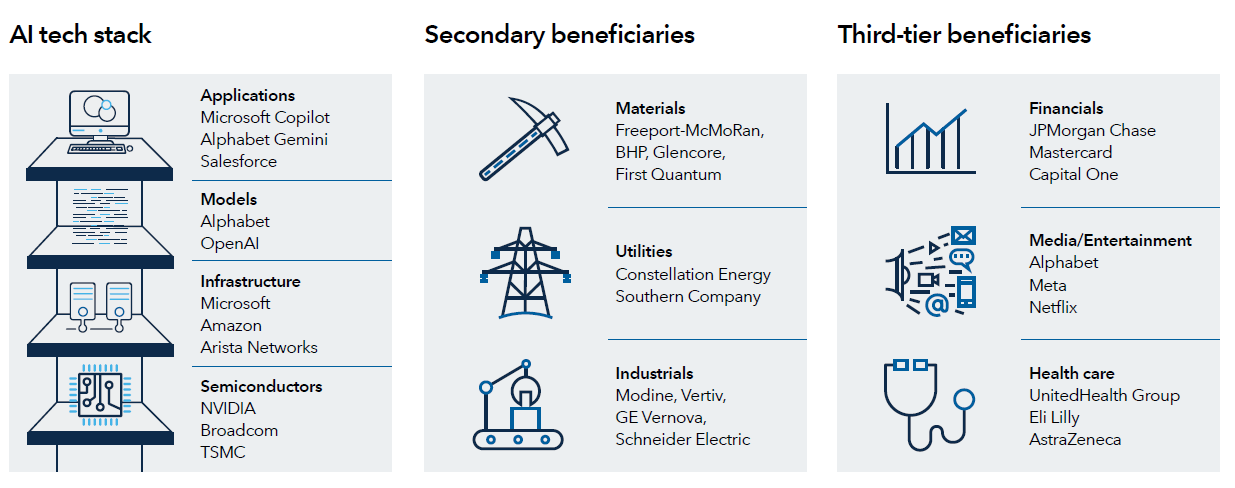

AI: From Hype to Habit

Artificial intelligence remained a dominant investment theme, but its narrative matured.

Q4 saw companies integrate AI tools to cut costs, enhance logistics, and drive innovation across industries. As Capital Group observed, “AI will become pervasive in most software and hardware — and there will be many types of robots”.

Infrastructure and utility providers powering AI adoption — from chipmakers to energy firms — became standout beneficiaries in Q4.

Dividends Regain Prominence

Dividend-paying equities also delivered in Q4. Companies with consistent payout histories provided stability amid policy and rate shifts, outperforming broad market averages during volatility.

Dividend aristocrats remain a core defensive strategy entering 2026.

Concluding Thoughts: The Balance Ahead

The final quarter of 2025 brought much-needed balance to a year defined by turbulence. Inflation eased, growth stabilized, and monetary policy turned supportive — a rare alignment after two years of volatility.

As we enter 2026, markets appear poised for moderation, not mania. The lessons of Q4 remain instructive:

• Resilience matters more than prediction.

• Diversification continues to work.

• Quality and discipline remain the investor’s edge.

If 2024 was a year of caution and 2025 one of adaptation, then 2026 begins as a year of equilibrium — where patient investors may finally be rewarded for staying the course.

As always, our team stands ready to help you review your allocations, explore opportunities, and ensure your portfolio remains aligned with your goals in this evolving environment.

Warm regards,

Your Wela Financial Advisory Team

Upcoming Client Events

Spring Cleaning, Shred-It Event, Saturday, April 11th at Wela Financial Advisory, 8 -11 a.m.

Bring any old documents to be securely disposed of and enjoy some breakfast tacos, doughnuts, and coffee!

Brent Forrest & Associates, LLC. dba Wela Financial Advisory (Wela) is a registered investment adviser. Information presented is for educational purposes only. It should not be considered specific investment advice, does not take into consideration your specific situation, and does not intend to make an offer or solicitation for the sale or purchase of any securities or investment strategies. Investments involve risk and are not guaranteed. Be sure to consult with a qualified financial adviser and/or tax professional before implementing any strategy discussed herein.