2025 Mid-Year Financial Insights

Dear Wela Clients,

We have crossed the midpoint of 2025 and are pleased to share the latest market observations and strategic ideas to help you navigate the second half of the year. In this edition of the newsletter, we examine six themes shaping portfolios today:

- Uncertainty as the new economic normal

- Tariff turbulence

- Lower growth expectations for H2 2025

- The Federal Reserve’s position on interest rates

- The Fixed-Income playbook

- Opportunities in equities

The Economy: Uncertainty Is the New Normal

Before we dive into asset classes, it is worth grounding ourselves in the single biggest macro-economic force shaping every portfolio decision this year: policy uncertainty. Tariff headlines, election-year rhetoric and rapidly shifting alliances now move markets as sharply as any jobs or GDP report. To understand how this climate affects growth and risk appetite, we first examine the evidence that uncertainty itself—rather than any one economic indicator—has become the dominant driver of sentiment.

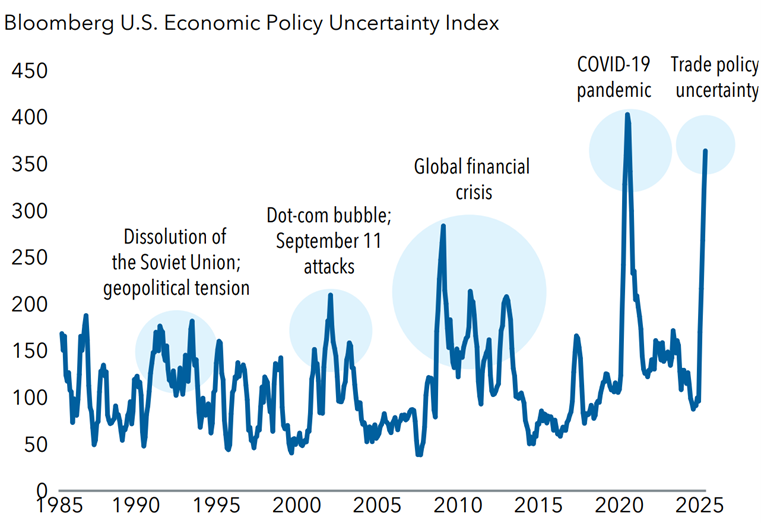

The Bloomberg Economic Policy Uncertainty (EPU) Index measures how often Bloomberg’s news wires simultaneously mention the words economy, policy and uncertainty. When the index climbs, it simply tells us that policy-related uncertainty is dominating the news cycle, a signal investors often treat as a cue to become more cautious.

The Index has surged to nearly 400, a level last seen during the pandemic, underscoring how fast-moving tariff announcements and shifting alliances are rattling corporate planning. For context the index is 100 points higher than during the 2007/08 global financial crisis.

The economy has entered a policy-driven grey zone where every tariff headline can jolt business plans and move markets as surely as a macro data release. With the Bloomberg EPU Index now flashing the same warning levels we saw during the pandemic, investors have little choice but to factor political brinkmanship into their outlook.

Tariff Turbulence: Why Headlines Matter Again

Tariffs are back in the spotlight because they sit at the heart of President Trump’s 2024-25 re-election platform, where he has pitched them as both negotiating leverage and an engine for “America-first” re-industrialization. Each fresh headline—whether announcing a new duty, an exemption or a retaliatory move—reverberates through supply-chain plans, earnings guidance and, ultimately, market sentiment.

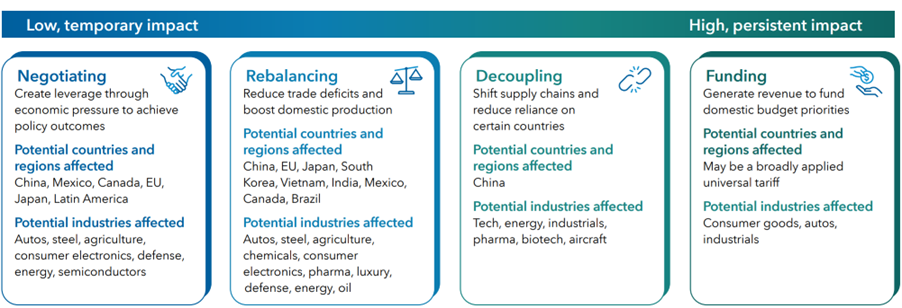

While tariffs now dominate the policy conversation, their objectives — and therefore their market consequences — vary widely. Our research suggests four distinct buckets:

● Negotiating chips: Temporary duties deployed to secure broader policy concessions, such as cooperation on immigration or drug enforcement, and usually rolled back once a deal is struck.

● Rebalancing levies: Reciprocal tariffs intended to narrow bilateral deficits and prod trading partners such as Europe, Japan and Mexico toward more symmetrical market access.

● Decoupling tools: Measures aimed at reducing reliance on single-source supply chains, particularly China, and encouraging the reshoring of strategic manufacturing.

● Revenue raisers: Duties levied primarily to generate funds that offset other policy moves, including tax relief.

“Understanding the motive matters,” notes Capital Group economist Jared Franz. “Negotiation tariffs tend to be fleeting, but those tied to long-term decoupling could stay in place for years.”

For investors, the key takeaway is to stay anchored in a disciplined, long-term plan while keeping enough flexibility to adapt when tariffs create genuine structural shifts or near-term dislocations. In short: use tariff-driven volatility as an opportunity—not a reason—to rethink fundamentals.

Lower Our Growth Expectations

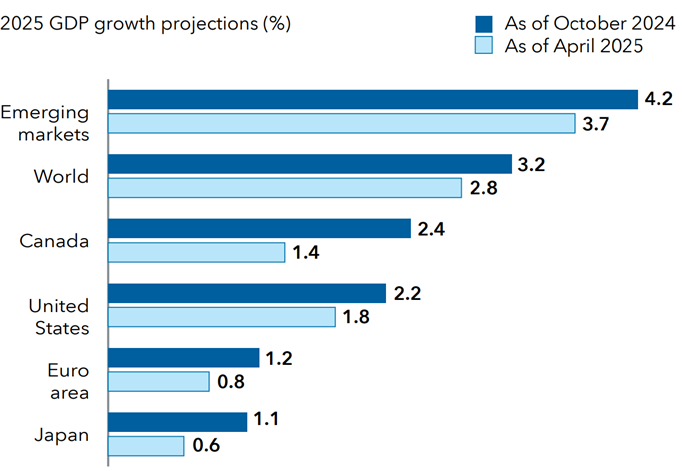

Uncertainty around U.S. trade policy—punctuated by ever-higher tariffs—has jolted the global economy. First-quarter U.S. GDP slipped for the first time since 2022, prompting many companies to withdraw guidance, postpone capital spending, watch cargo volumes at major ports collapse and put hiring on ice.

Reflecting this policy fog, the IMF has already trimmed growth forecasts for the United States, Europe, Japan and many emerging markets.

Limited trade accords among the U.S., U.K. and China provide a glimmer of progress, yet, as Capital Group economist Darrell Spence observes, companies have “hit the pause button” until the rules of engagement come into focus—a hiatus that may or may not tip the economy into recession but unquestionably lifts the risk.

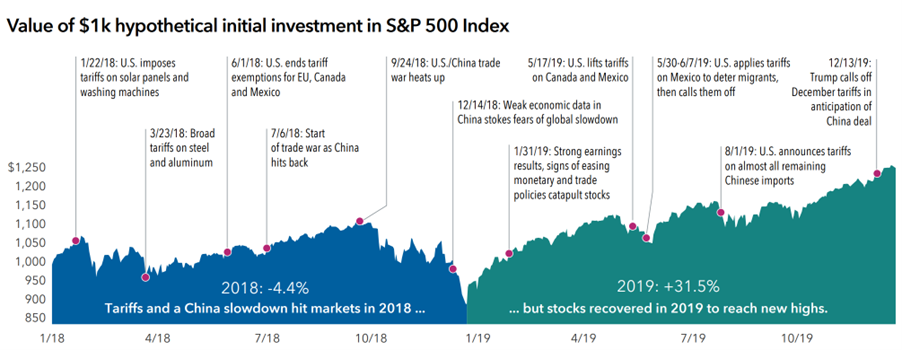

We have seen this movie before.

During the 2018–19 trade war, equity markets sold off hard and then rebounded once negotiations gained traction. Today’s policy backdrop is broader—touching national security, energy and supply chains—but the lesson is similar: volatility can create entry points for long-term investors.

Amid economic uncertainty and slower growth expectations, investors are looking to the Federal Reserve for guidance.

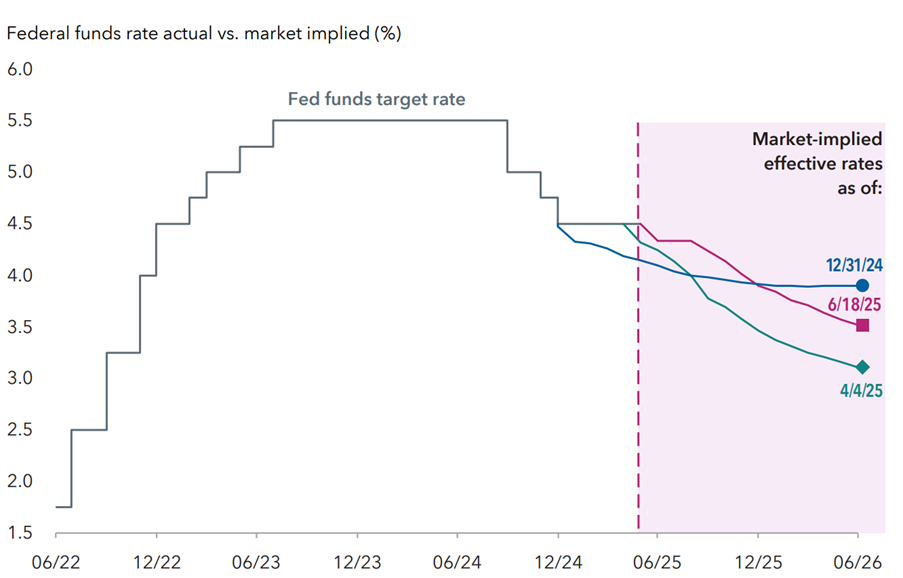

All Eyes on the Federal Reserve

Borrowers may be eager for a reprieve, but the Federal Reserve appears content to keep policy rates in a holding pattern until it can gauge the economic fallout from the latest tariff salvo.

“With the labor market still firm and inflation hovering above target, the Fed has every incentive to stay patient,” observes portfolio manager Chitrang Purani, who sees a year-end policy rate near 3.8% as a reasonable midpoint. Even if negotiations dilute some of the new duties, the broader forces of de-globalization and policy unpredictability are likely to drag on near-term growth.

Should market functioning wobble — as it did in the early days of the pandemic — the Fed retains ample tools to inject liquidity. At the same time, trade-driven volatility, a recent Moody’s downgrade of U.S. sovereign credit and persistent fiscal deficits have begun to erode Treasuries’ “risk-free” aura, suggesting investors may soon demand a richer premium to hold them.

The Fixed-Income Playbook: Income-Backed Resilience

Against this backdrop of a patient—but far from passive—Federal Reserve, our fixed-income playbook pivots on one core idea: harvest dependable income while keeping portfolios agile enough to weather further policy surprises.

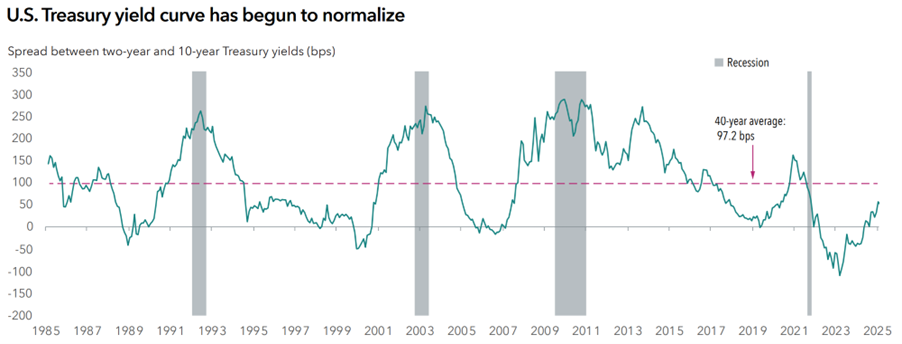

● Treasuries: The modest re-steepening of the Treasury curve now rewards investors who ladder maturities; we favor holding a barbell of short bills for liquidity and selectively adding long bonds as “convexity insurance” should growth falter.

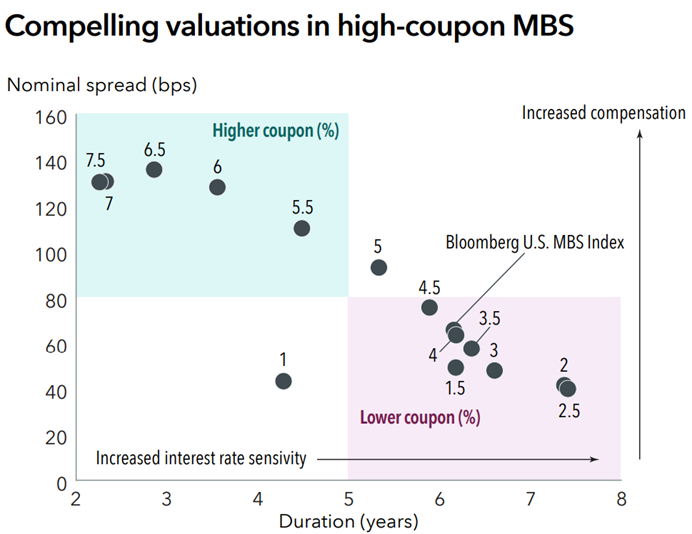

● MBS: For carry without excessive duration, we look to high-coupon agency mortgage pools and other securitized assets, where government or senior-tranche protections help dampen volatility while spreads remain compelling.

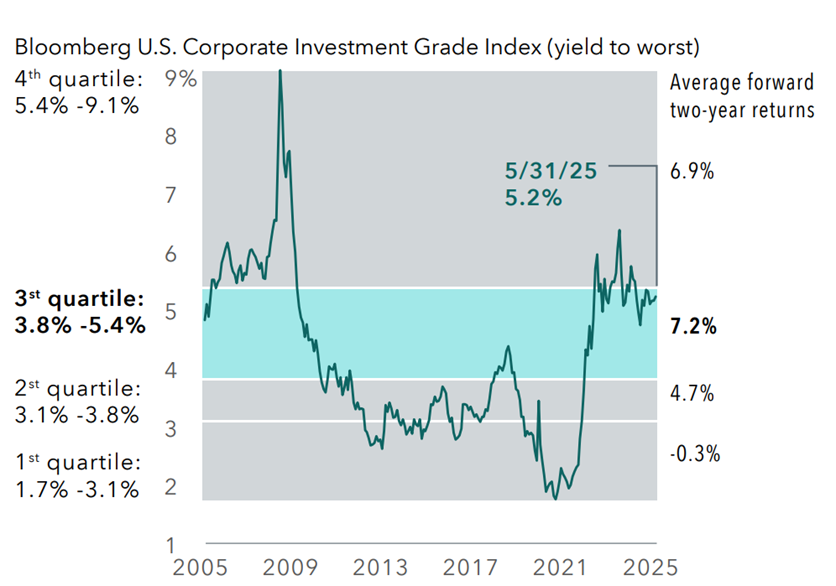

● Corporate Bonds: In corporate credit, starting yields north of ~5%* in investment-grade and ~7–8% in high-yield space have historically translated into mid- to high-single-digit forward returns—especially when issued by companies with manageable near-term refinancing needs.

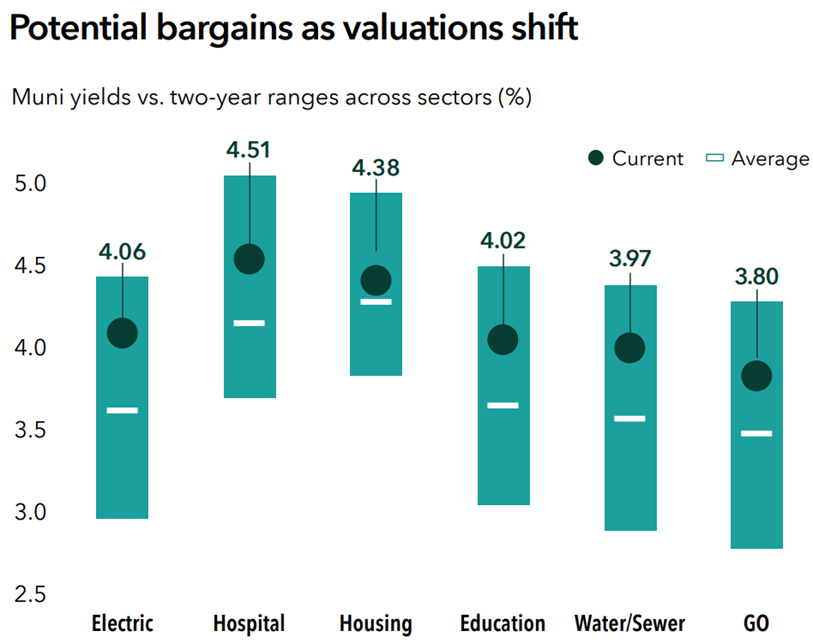

● The return of Munis: Tax-equivalent yields in the municipal market now rival BBB corporates, and the unusually kinked municipal curve lets investors extend duration on favorable terms while preserving credit quality.

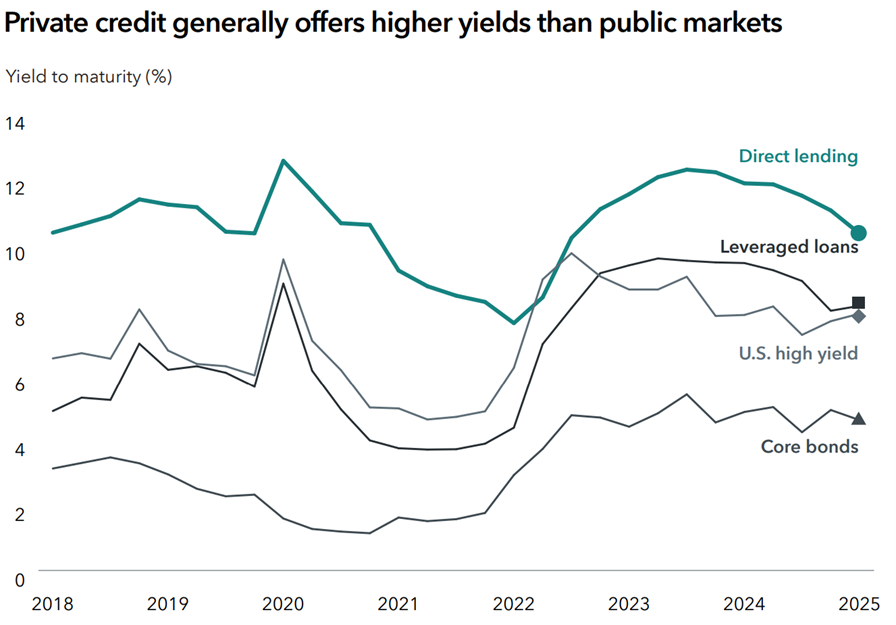

● Private Credit: Finally, although private-credit spreads have tightened, direct-lending and asset-backed finance still offer a robust liquidity premium for disciplined underwriters who can structure covenants and collateral effectively.

Taken together, this multi-layered bond strategy is designed to let investors collect attractive income today while preserving the flexibility to pivot tomorrow—ensuring portfolios stay both resilient to policy shocks and positioned to capture opportunity as the rate cycle evolves.

Equity Opportunities: Pick Your Sector

With the bond market positioned to present steady income and cushion policy shocks, the next lever for portfolio growth lies on the equity side. Tariff turbulence has created pockets of mispricing, while secular investment themes—from national security spending to AI-driven cap-ex—continue to gather momentum. The result is a market where fundamentals—not index weight—should drive allocation decisions.

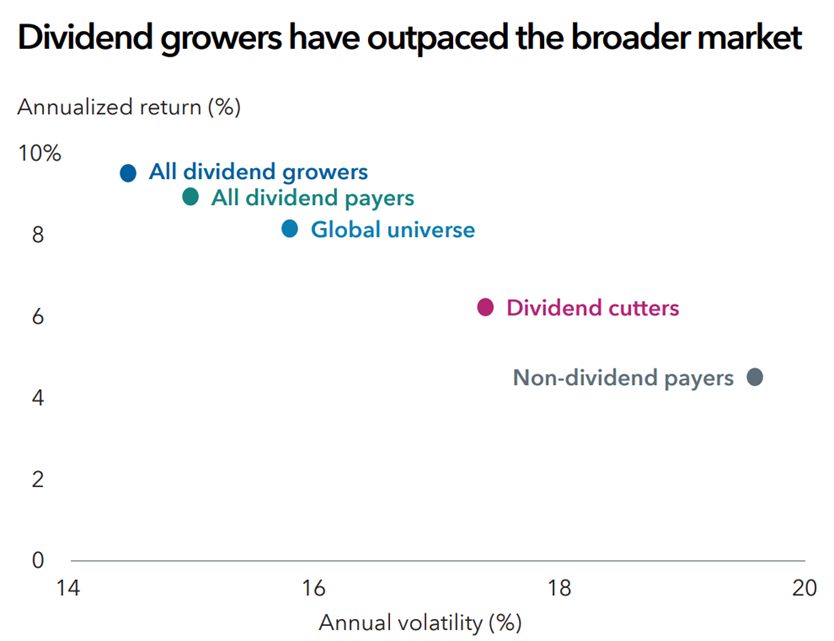

● Dividend Shields: Companies that have grown dividends year after year have delivered higher returns with less volatility than both the broader market and the wider universe of payers. Examples include CenterPoint Energy, KPN and Intact Financial, all of which continue to raise payouts despite trade uncertainty

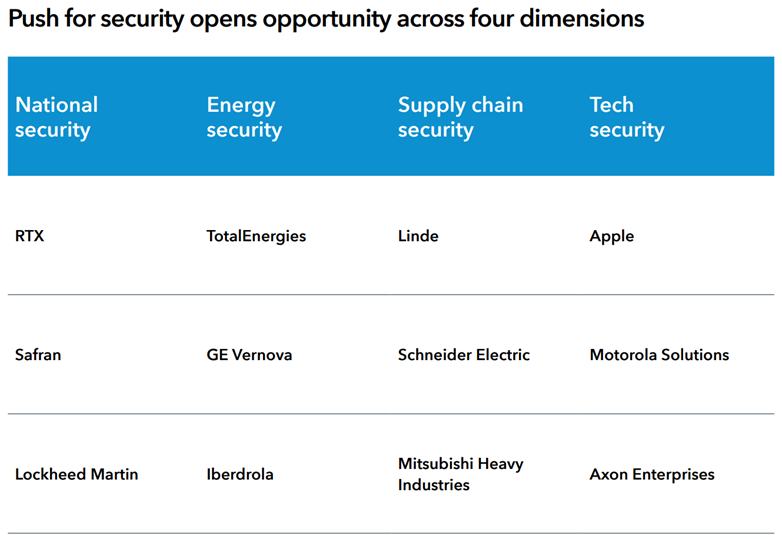

● Security Takes Center Stage: Governments worldwide are boosting spending on national, energy, supply-chain and tech security. Beneficiaries span defense primes such as Lockheed Martin and grid-modernization leaders like Siemens Energy and GE Vernova.

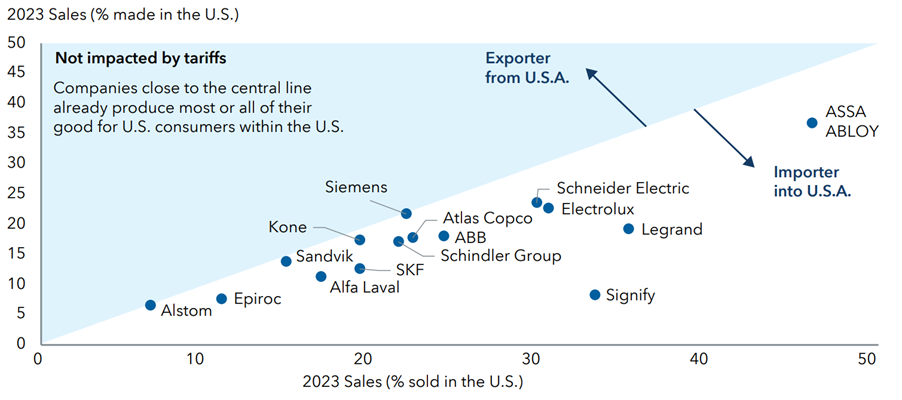

● Multinationals Go “Multi-Local”: Many global firms are moving production closer to end markets. Siemens’ new Texas plant and Apple’s planned $500 billion U.S. build-out illustrate how multinationals can sidestep tariffs and still thrive.

● Valuation Resets & Secular Growth: Sharp selloffs have repriced leaders in semiconductors (critical for AI capital expenditures), GLP-1 weight-management therapies and travel/leisure—sectors that historically bounce back once panic subsides.

Selective exposure to these four clusters can convert today’s dislocations into tomorrow’s compounding. We continue to favor diversified baskets of high-quality stocks—anchored by reliable dividend growers and complemented by targeted secular themes—while remaining nimble enough to add or trim as trade negotiations and earnings trajectories evolve. In short, disciplined stock selection, backed by fundamental research, is the best antidote to policy-driven volatility.

Concluding Thoughts

Volatility is the entry fee investors pay for long-run returns. By focusing on income durability, strong balance sheets and secular growth themes, disciplined investors can convert today’s dislocations into tomorrow’s compounded gains.

Periodic rebalancing—prompted by shifts in your objectives, meaningful changes in fundamentals, or tactical pockets of value—allows us to trim where valuations look stretched and add where risk-adjusted returns have improved.

If you’d like to discuss how these principles apply to you specifically, please reach out and we are here and happy to help!

Warm Regards,